Methodology of Study

To validate the size of the worldwide urgent care centre market and estimate the size of other dependent submarkets, top-down and bottom-up methodologies were utilised. The World Health Organization, the Centers for Disease Control and Prevention, the World Heart Federation, the Society for Cardiovascular Angiography and Interventions, the American College of Cardiology, the American Heart Association, the European Association of Percutaneous Cardiovascular Interventions, the Urgent Care Association of America, directories, industry journals, databases, and company annual reports were all used to identify the patients. To gather and validate information as well as assess the dynamics of this market, primary sources such as specialists from both the supply and demand sides were interviewed.

[Report: 132 Pages] The worldwide urgent care centre market was worth USD 19.20 billion in 2017 and is expected to grow at a CAGR of 5.3 percent to USD 25.93 billion by 2023. The report’s base year is 2017, and the projected term is 2018–2023.

Get PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=197843477

Business Information

Additional market players will be profiled and analysed in detail (Up to 5)

The global urgent care centre market is expected to grow at a CAGR of 5.3 percent to USD 25.93 billion by 2023, up from USD 20.07 billion in 2018. Factors driving this market’s growth include increased investments in urgent care, an ageing population, strategic partnerships between urgent care providers and hospitals, and affordable care and shorter wait times provided by urgent care centres.

The research examines the global market in terms of service, ownership, and region. It includes thorough information on the primary variables influencing market growth as well as regulatory analysis that affects market dynamics.

Acute sickness care, trauma/injury treatment, physical examination, vaccinations & vaccination, and other services (diagnostics, telemedicine, and travel & occupational medicine) make up the global market. During the projection period, the trauma/injury treatment segment is predicted to grow at the fastest rate. The strong rise in this area might be linked to an increase in the frequency of unintended, small injuries as well as a growing preference for economical, readily available healthcare.

The market is divided into corporate-owned, physician-owned, hospital-owned, and other centres based on ownership. There are two types of physician-owned urgent care centres: multiple physician-owned and single physician-owned. During the projection period, the corporate-owned urgent care facilities category is predicted to account for the greatest share and have the highest CAGR.

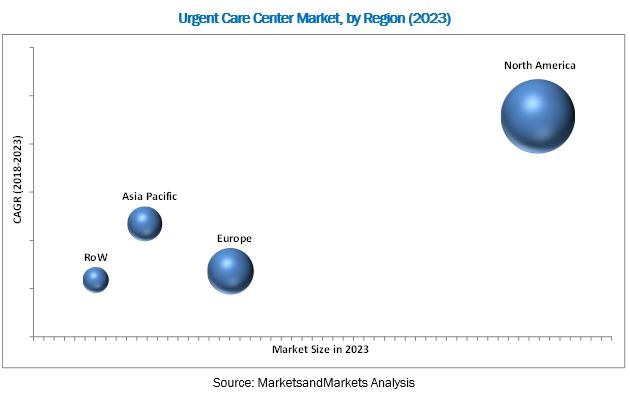

North America, Europe, Asia Pacific, and the Rest of the World are the geographic segments covered in this report. In 2018, the North American sector is predicted to have the greatest share of the market. The region’s huge proportion and rapid expansion can be linked to the region’s expanding senior population, the accessibility and cost of urgent care services, and the introduction of specialist urgent care.

Get a Sample :

https://www.marketsandmarkets.com/requestsampleNew.asp?id=197843477

Key Market Players

Lack of a skilled workforce could be a challenging factor for this market. Concentra (US), MedExpress (US), American Family Care (US), NextCare Holdings (US), and FastMed Urgent Care (US) are the key players in the Urgent Care Center Market. Other players involved in this market include CityMD (US), CareNow Urgent Care (US), GoHealth Urgent Care (US), HCA Healthcare UK (UK), Columbia Asia Hospitals (India), International SOS (China), and St. Joseph’s Health Care London (Canada).